How student loan debt became a trillion-dollar problem for Americans

[ad_1]

CNN

—

Millions of Americans have student loan debt, amassing to more than $1.6 trillion by the end of last year, according to the Federal Reserve Bank of New York.

It’s the result of a decades-long explosion in borrowing coupled with soaring education costs.

The Federal Reserve data shows people under the age of 30 are more likely to have student loan debt compared with older adults – underscoring the crippling burden on another generation of Americans.

But the impact is multigenerational. Nearly a quarter of the outstanding student loan debt is owed by Americans who are 50 and older.

College graduates do earn more than those who do not have a degree. In 2021, full-time workers age 25 and older with a bachelor’s degree out-earned those with a high school diploma and no degree by about $27,000 annually, when comparing median salaries, according to data from the Bureau of Labor Statistics.

But these high-paying jobs come at a price. In the 2020-2021 academic year, the College Board found that 51% of students who graduated from public four-year institutions left with federal debt averaging more than $21,000 per person. That figure is slightly higher for those who went to a private institution, with 53% graduating with federal debt averaging more than $22,000.

College costs have soared, outpacing the inflation rate, according to Mamie Voight, the president and CEO of the Institute for Higher Education Policy.

In the 1968-1969 academic year, adjusted for inflation, it cost $1,545 to attend a public, four-year institution, according to data from the National Center for Education Statistics. This includes tuition, fees, room and board. That’s compared with $29,033 in the 2020-2021 school year, data shows.

If education costs remained in line with inflation, that number would be around $12,000 per year.

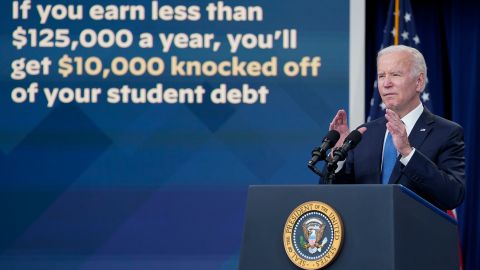

President Joe Biden’s federal student loan forgiveness program is offering some relief for millions of people. It calls for granting up to $10,000 of federal student loan debt relief for qualifying borrowers. Those who received a Pell grant in college could be eligible for an additional $10,000 in relief.

But no debt has been canceled yet. The plan was put on hold indefinitely as legal challenges work their way through the courts. The Supreme Court will hear arguments Tuesday in two cases concerning the forgiveness program, with a decision expected by late June or early July.

Student debt has not always been a crisis. The modern federal education borrowing system came from a series of legislative moves aimed at helping more people have access to college – but it came with some unintended consequences.

1958: The first federal initiative

The National Student Loan program, aimed at expanding access to higher education, was launched in 1958. Created from the National Defense Education Act, it was the first federal student loan initiative for those studying certain subjects to improve science, mathematics and engineering skills during the Cold War.

1965: Higher Education Act

The Higher Education Act of 1965 opened the possibility of college to even more people, regardless of area of study – but it also created a new type of relationship between the federal government, banks and college campuses through the Guaranteed Student Loan program.

“The Guaranteed Student Loan program is really the big original student loan program, and it was modeled off the mortgage program,” said Elizabeth Shermer, a historian and associate professor at Loyola University Chicago who has researched and written about student loans.

It solved for the government the challenge of how to get lenders involved with such a risky financial investment: The loan did not come from the federal government, but instead, the government assured repayment to bankers willing to give loans, Shermer said.

Using the federal mortgage program as a guide allowed the government to avoid direct investment into colleges, she said, but mortgages and student loans are not the same. The federal government cannot take away your degree in the same way a bank can repossess your house.

“Instead, this assumption being that it is un-American to have a free ride, so we will use the lending that turned a country of renters into a nation of homeowners. But just like we now know how the mortgage program exacerbated racial and gender inequality, the same thing happened with the student loan programs too,” she said.

1970s: Sallie Mae and a boom in borrowing and private loans

The 1970s were a turning point for federal debt. Federal loans rose quickly due to the formation of new, private loans and the pressure to cut taxes.

The Student Loan Marketing Association, known as Sallie Mae, was created through the reauthorization of the Higher Education Act in 1972.

Modeled from Fannie Mae, a program created during the Great Depression that made it easier to buy and sell mortgage debt in order to create more reliable funding for housing, Sallie Mae started offering private student loans along with other financial products.

“It makes it more profitable to be a part of it because you can buy and sell student debt, just like you could mortgage,” Shermer said.

This was the “most important” moment in the history of loans, she said, as the availability of financial aid products to both for-profit and nonprofit companies allowed for the rise of private student loans.

That coupled with the rising cost of tuition in the 1970s meant that students needed more money to continue their education. Since there was a limit to how much students could borrow in federal loans, private loans were needed as a supplement.

“It really is going to be this expectation that you are going to need to borrow something to get through college,” Shermer said. “It’s like that perfect storm,” she added.

Another reason why private loans became more critical was pressure in Washington for Congress to cut taxes and cut spending, she said.

“As every legislature knows, if you cut the appropriations for higher education, colleges and universities can just increase what they charge. Just increase tuition,” Shermer said.

1990s: Direct loans

To fix the issues caused by modeling student loans on mortgages, the William Ford Direct Student Loan program, or the Direct Loan Program, was enacted in 1992. It eventually replaced the Guaranteed Student Loan program. Instead of just reassuring banks that they would be paid back, the US Department of Education directly gave loans to students.

“After it was discovered how poorly managed this thing was run – after one of the student lenders went bankrupt – they had this idea and noticed that it would actually be cheaper for the federal government to just lend directly to students and parents,” Shermer said.

Loans direct to students were not only more cost-efficient, but they were also cheaper for borrowers and easier for campuses to use, she said.

Other initiatives

In the intervening years, several initiatives were launched aimed at reducing the rate of default. The Income-Contingent Repayment Plan, or ICR, of 1993 capped payments for qualified borrowers at 20% of their discretionary income or 12 years of fixed payments, whichever was lower, according to the Institute for Higher Education Policy and the Lumina Foundation.

Another type of income-driven repayment plan, the Income-Based Repayment Plan, or IBR, was created in 2007. It lowered payment caps to 15% of discretionary income and forgave the balance of loans after 25 years of payments.

The Pay As You Earn program, launched in 2010, provided the guidelines many borrowers still use today – capping payments at 10% of discretionary income and cancellation of loans after 20 years.

August 24, 2022: The Biden plan

The Biden administration announced the federal student loan forgiveness plan, which if allowed to move forward, will grant up to $20,000 in debt relief.

Biden also announced a new income-driven repayment plan aimed at making repayment more manageable.

Even if the one-time loan forgiveness program is rejected by the Supreme Court, the proposed repayment plan is less likely to face the same legal challenges.

The plan would cap payments at 5% of the borrower’s discretionary income, create a shorter time to forgiveness and cover unpaid monthly interest when balances are low.

The Department of Education expects to start implementing some parts of the new income-driven repayment plan later this year. But first, the proposal is going through a formal rulemaking process, having received more than 13,000 public comments, and changes may be made to the proposal before it takes effect.

[ad_2]

Source link